With a home-equity conversion mortgage, seniors can finance the purchase of a new home without monthly payments

Source: A Reverse Mortgage to Buy a Home? Here’s How – WSJ

With a home-equity conversion mortgage, seniors can finance the purchase of a new home without monthly payments

Source: A Reverse Mortgage to Buy a Home? Here’s How – WSJ

![]()

It is my pleasure to specialize in the origination of Home Equity Conversion Mortgages (HECM) for the benefit of our clients. These are best known as Reverse Mortgages. The type of Reverse Mortgage we offer, and the most utilized product available in Colorado, is the one insured by the Federal Housing Administration (FHA) of the US Department of Housing and Urban Development (HUD) as further discussed by the Federal Deposit Insurance Corporation (FDIC) and as discussed by the Consumer Financial Protection Bureau (CFPB).

DISCLAIMER: This publication does not represent that any of the information provided is approved by HUD or FHA or any US Government Agency.

DISCLOSURE: The information provided herein is not intended to be an indication of loan approval or a commitment to lend. Additional program guidelines may apply. Information is subject to change without notice.

Financially Speaking™ James Spray MLO, | CO LMO 100008715 | NMLS 257365 | Updated May 8, 2022

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct for your situation. This information is not legal advice and is for guidance only. You may reproduce this information in whole and not in part, providing you give full attribution to James Spray.

The following is not written as an extensive discussion about the roles of mortgage lenders or mortgage servicers. Rather it is written to provide a brief and very general overview of these two different and separate functions within the residential mortgage industry.

Quoting from the CFPB, “Your mortgage lender is the financial institution that loaned you the money. Your mortgage servicer handles the day-to-day tasks of managing your loan. Your loan servicer typically processes your loan payments, responds to borrower inquiries, keeps track of principal and interest paid, manages your escrow account, and may initiate foreclosure if you miss too many loan payments. Your servicer may or may not be the same company that gave you your loan.” In other words, the mortgage lender may also be the mortgage servicer.

How does the mortgage lender get paid? The mortgage lender may get paid with a combination of an origination fee and the spread between the interest rate paid for the funds it lends and the interest rate charged to the borrower for those funds. Or the mortgage lender may just get paid on the spread between the interest rate paid for the funds and the interest charged to the borrower for those funds.

How does the mortgage servicer get paid? Generally speaking, there are four streams of income for the servicing function.

First, the servicer gets a servicing fee. The servicing fee is typically calculated as a percentage of the outstanding principal balance of the loans serviced. Generally speaking, it is interest on the principal which ranges between one-eighth (0.125) and one-half (0.50) percent and which is retained by the servicer.

Second, the servicer is entitled to keep the “float” on the mortgage payments received. To illustrate: the borrowers remit payments to the servicer on the first of the month, however the servicer is not be required to remit the funds to the lender/mortgagee until the end of the month. The result is that the servicer gets use of the funds for the most of the year with the exception of the few days each month when the servicer must remit to the lender/mortgagee.

Third, the servicer retains any supplementary fees it collects. The promissory note of the mortgage specifies the amount and payment of late fees as well as any other fees or costs related to the collection of late fees.

Finally, the servicer earns revenue from the fees and interest generated by funding mortgage servicing advances.

Financially Speaking™ James Spray, RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct for your situation. This information is not legal advice and is for guidance only. You may reproduce this information in whole and not in part, providing you give full attribution to James Spray.

Official Device To Prove Future Income

2014 > Qualified Mortgage (QM) or Qualified Residential Mortgage (QRM) Lending Documentation Requirements and,

Ability To Repay (ATR) Documentation Requirements:

Verified minimum of previous 24 months wage earner employment or,

Confirmed previous 24 months self-employed (no blending of self-employed with wage earner); we’ll call this the Bernake syndrome. The former Federal Reserve chairman, speaking in Chicago told the moderator: “just between the two of us, I recently tried to refinance my mortgage and I was unsuccessful in doing so.”The lender must establish the likelihood of continued employment/income for the next 36 months.

The QM/QRM rule became effective on January 10, 2014. Residential mortgages subject to Reg. Z (1-4 unit owner-occupied homes) require the borrower’s income/assets are to be fully documented and verified.

Asset and Other Income Documentation

Standards

In the present regulatory climate many lenders impose underwriting rules (referred to as “overlays”) that are more restrictive than required by law or regulation. One set of overlays: bankruptcy, foreclosure, short-sale and deed-in-lieu of foreclosure prevent entry or reentry to the mortgage market for certain time periods as displayed here. Points and fees which may charged to borrowers are defined and limited. For the details, click here.

Exceptions to QRM and ATR

Investment properties are exempt. These are provably non-owner occupied residential properties. The proof is provided with 1040’s and schedules as well as the income shown with bank statements and an accompanying lease agreement. Credit Unions and banks serving underserved communities also have certain exemptions. As well, there are non-QM loans which do not feature low down-payment options or highly favorable rates and terms.

Media outtakes/observations from the industry biased view:

“…lenders are imposing higher than usual credit scores and other tough standards on people applying for government-backed mortgages. The lenders say they’re exceeding the government’s own criteria in a bid to insulate themselves from more financial penalties and lawsuits. And several analyses suggest that millions of potential home buyers are getting shut out as a result.” The Washington Post recently published: Why the next pick for U.S. Attorney General has huge implications for the housing industry.

Critique: For a well thought critical observation of potential serious failures of the discussed reforms, read QRM’s Missed Opportunities for Financial Stability and Servicing Reform by Alan Levitin. Mr. Levitin states in part that “… QRM was (a) missed chance to fix servicing for both investors and consumers.”

*On FICO® Scores, the best rates at the lowest cost are available for borrower with a minimum 740 middle score based on the FICO® models used by lenders which are also used by Fannie Mae and Freddie Mac. With lower scores one may expect a higher rate with additional underwriting overlays such as lower DTI and LTV, more liquid assets and higher down payments among other overlays.

Financially Speaking™ – James Spray, RMLO, CNE, FICO Pro CO LMO 100008715 | NMLS 257365 |Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.

For this post, we are simply quoting from other media sources to help our readers understand the new FICO 9 credit scoring model. In spite of what you may have read, the FICO 9 credit scoring model will not help significantly, if at all, with home mortgages. At least not anytime soon. FICO 9 will be utilized sooner by vehicle and credit card lenders.

On August 23, 2014, The Motley Fool published Why New FICO Score Rules Could Be a ‘Game-Changer’ In Helping You Obtain a Loan stating, in part, the following: “According to FICO, the median FICO score for consumers whose only major derogatory references are unpaid medical debts is expected to increase by 25 points.

FICO’s new more lenient model should also benefit collection agencies. Consumers with unpaid medical debts now have an incentive to settle, knowing that FICO will stop including in its calculations any record of a consumer failing to pay a bill, if the bill has been paid or settled with a collection agency.

Auto and Credit Card Lenders Will Be First to use FICO 9

“This is great news for collection agencies,” Rood said. “It provides laggards with an incentive to pay up. Before these changes, you were incentivized not to pay off your debt. The last thing you wanted to do was trigger a new ‘date of last activity’ report for an old debt, say, a debt from 2008. Again, you were just better off not paying it because older debts weighed less heavily against you on your credit report than new debt. The new scoring model will likely be implemented by credit card and auto lenders first. Mortgages typically lag in adopting new scoring models.”

Mortgage Lenders Will Be Last to use FICO 9

The New York Times in their article of August 7, 2014 titled: Credit Scores Could Rise With FICO’s New Model explained it very well. “For consumers to see any benefit, however, lenders have to adopt the new scoring techniques. FICO last introduced a new model, called FICO 8, in 2008. Since then, FICO said that about half of its customers had started using that model.

Mortgage lenders have been slower to adopt new scores, and most are using even older versions, experts said, because Fannie Mae and Freddie Mac are still using them in their own underwriting software. Fannie and Freddie did not say whether they had plans to switch to the updated FICO score that weighs medical collections less heavily. But they both said they were confident in the tools they use.”

Finally, law professor and author James Kwak, states the facts very simply: “…the financial district of the Western societies, Wall Street, and outdated software may very well be the norm not an exception.”

The Take Away

The take away on all this, according to Ted Rood of the Mortgage News Daily is that “(home and mortgage) buyers should keep paying those medical bills and avoid collections to ensure their loan approvals!” This statement was excerpted from the article titled: New Credit Score Model Would be Great for Housing! Too Bad it Won’t be Used.

Final Word

Our regular readers already know of our thoughts on FAKO credit scores and the release of FICO 9 adds yet a new dimension. Consumers purchasing their scores from the myFICO site will get real FICO scores but they are likely not going to be the scores which mortgage lenders use. So what can you do? You can write or call elected officials and ask that they help Fannie Mae and Freddie Mac catch up with the times.

More on FICO 9 from the FICO Blog.

UPDATE: 09/22/15 | GSEs Struggle to Update Credit Scoring Models

Financially Speaking™ James Spray, RMLO, CNE, FICO Pro CO LMO 100008715 | NMLS 257365 |September 23, 2014 | Updated September 22, 2015 Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.

Fannie Mae updated its policies regarding significant derogatory credit events, which in some cases allows more borrowers to reenter the housing market. These updates are reflected in the embedded chart: How long after bankruptcy or foreclosure must you wait to get a mortgage?

The borrower is now held to the bankruptcy waiting period (4 years) and not the foreclosure waiting period (7 years). This is true even if a foreclosure action is subsequently completed to reclaim the property in satisfaction of the debt. This is a significant and favorable change. From the FNMA underwriting guidelines [B3-5.3-07, Significant Derogatory Credit Events — Waiting Periods and Re-establishing Credit (08/07/2019)]: “Foreclosure and Bankruptcy on the Same Mortgage If a mortgage debt was discharged through a bankruptcy, the bankruptcy waiting periods may be applied if the lender obtains the appropriate documentation to verify that the mortgage obligation was discharged in the bankruptcy. Otherwise, the greater of the applicable bankruptcy or foreclosure waiting periods must be applied.”

[At this time FHA/VA/USDA require a two year waiting period following discharge and a three year period post-foreclosure.]

The waiting periods are being updated to establish a standard four year waiting period, with a two year waiting period permitted providing a borrower has extenuating circumstances*.

[FHA/VA/USDA require a three year waiting period following Short Sale or Deed-In-Lieu.]

As a new policy, charge-offs of mortgage accounts now require a four year waiting period following this derogatory credit (two years if the borrower can demonstrate extenuating circumstances*).

Number one became effective July 29, 2014; two and three are effective for mortgage loans with applications dated on and after August 16, 2014.

How do you know if Fannie Mae owns/owned your mortgage? Click on FNMA Loan Lookup.

Based on past experience, it will take time for the mortgage origination industry to catch up with these new policies. Further, it is likely that some will not accept these policies within their own underwriting guidelines.

*Given the reliance on automated underwriting for compliance purposes, few lenders will delve into the perceived risk of manually underwriting extenuating circumstances for fear of losing the QRM safe harbor. QRM standards were implemented on January 10, 2014. The vast majority of lenders are staying squarely inside the New Rules box, so to speak.

Reference: Fannie Mae Selling Guide Announcement SEL-2014-10

Image Credit: Reuters/Jonathan Ernst

Financially Speaking™ James Spray, MLO, CNE, FICO Pro CO LMO 100008715 | NMLS 257365 |August 10, 2014 | Updated September 5, 2020Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.

New Rule on Reverse Mortgages

A new rule has been issued which allows that a reverse mortgage (HECM) shall protect borrowers even when one spouse is younger than 62. Both the purchase or traditional reverse mortgage amount will be based on the younger spouse’s age. Given the number of variables, and the complexity with how these new factors work please contact your trusted reverse mortgage loan originator.

For all FHA case numbers issued on or after August 4, 2014 this revolutionary new rule becomes effective. This rule will allow younger spouses of borrowers that no longer live in their home to stay in their home without the threat of foreclosure. In a nutshell, the requirements are this:

Prior to August 4, 2014, the full repayment of the reverse mortgage was due and payable following the death of the borrower, leaving the surviving spouse whose name was not on the mortgage in the lurch for the debt or forced to sell the home. This change defers that settlement until after the surviving spouse’s death.

This new rule comes at a cost. Lenders factor in the age of the younger spouse when calculating the reverse mortgage payout; in a nutshell, the younger the spouse the longer the loan will be outstanding resulting in the lesser payout.

Reference: FHA Mortgagee Letter: ML 2014-07

Readers of this blog may also wish to read: What Is A Purchase Reverse Mortgage? as well as The New Reverse Mortgage.

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.

Federal Reserve Board Building

QWR: The RESPA Letter

Most reading this post are reading it for a particular reason which is to learn about writing a letter to a mortgage lender and/or servicer regarding a specific problem or situation such as requesting the mortgage servicer report your payments to the credit bureau(s). For some, it may be that your mortgage servicer or bank is reporting incorrect information or you may need specific documentation. For others, perhaps this is being read for informational purposes. In any event, we trust the reader finds this information helpful.

Step 1. Contact your mortgage servicer for the correct address for legal correspondence. You must use the legal (registered) address of the servicer. Some servicers actually have a specific address for a Qualified Written Request (QWR). This is a different address than where you mail the payment or from where you get the periodic statements or notices. This procedure was established per the Real Estate Settlement Procedures Act (RESPA).

Step 2. You may utilize the following template provided by HUD for your QWR. Or you may click here to open and read the information or you may copy and paste the pertinent paragraphs (opening and closing) as show below. Focus your thoughts and keep your letter brief and specific to the topic.

“Attention Customer Service:

Subject: [Your loan number]

[Names on loan documents]

[Property and/or mailing address]

This is a “qualified written request” under Section 6 of the Real Estate Settlement Procedures Act (RESPA).

I am writing because:

Sincerely, [Your name – Printed and Signed]

I understand that under Section 6 if RESPA you are required to acknowledge my request within 20 business days and must try and resolve the issue within 30 business days.”

If you are satisfied with the resolution to your situation, you may wish to compliment the servicer by sending a note to the Consumer Financial Protection Bureau (CFPB or Bureau) via their Comment Form.

Step 3. Send your QWR via Certified Mail Return Receipt. Keep copies of your letter and any enclosures as well as your Certified Mail Receipt from the post office and the Return Receipt from your mortgage servicer proving they have received your QRM

Finally, if you are still unable to resolve the situation, there is a complaint process that may get action. We suggest this be your last and not first step as you will then have evidence which will indicate to the Bureau that the servicer is either unwilling or unable to address your situation. Mortgage Complaint Form

There’s a New Sheriff in Town

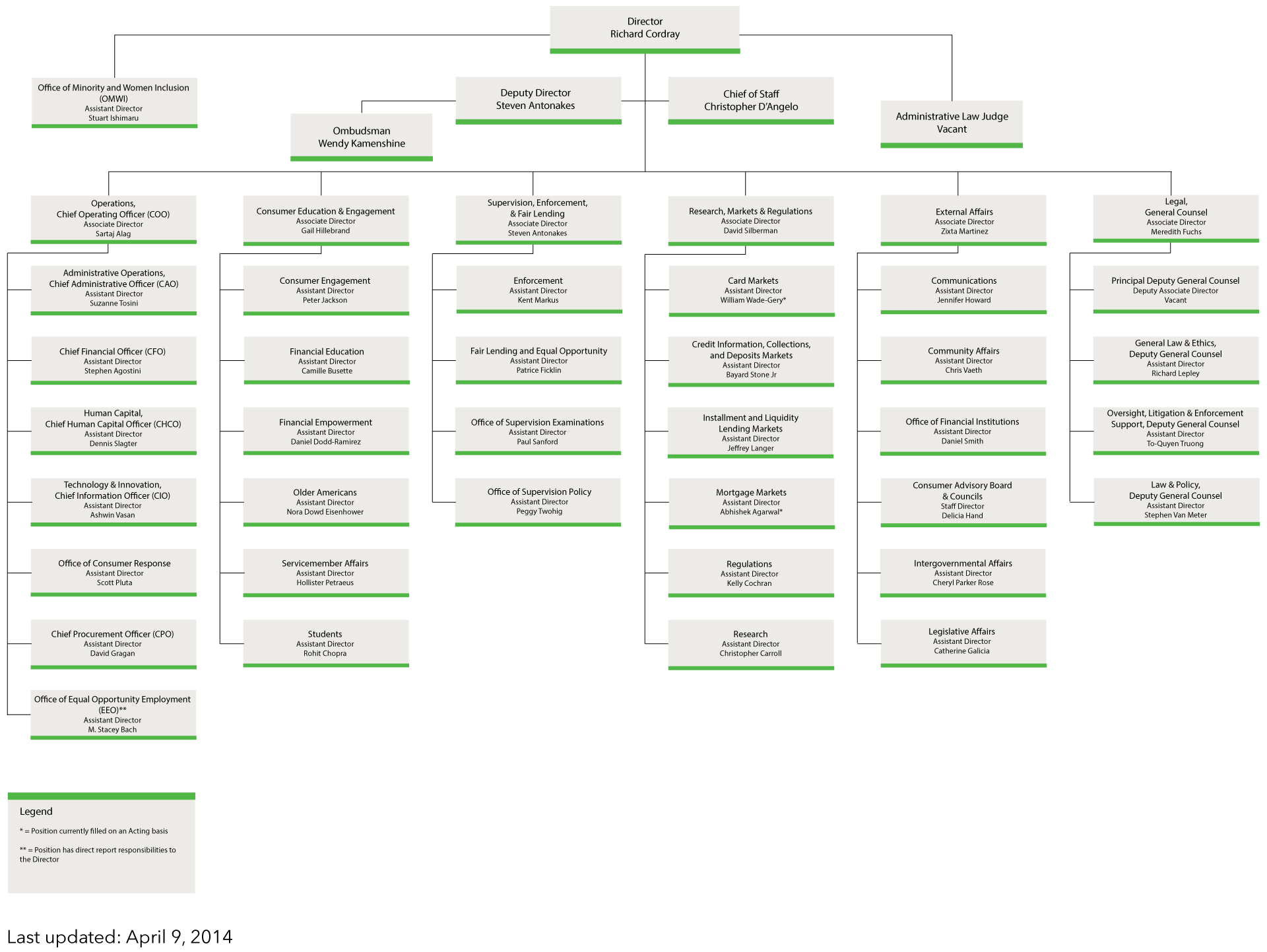

The following is excerpted from the prepared remarks of Steven Antonakes, Deputy Director of the CFPB which he presented to the Mortgage Bankers Association National Mortgage Servicing Conference in Orlando, Florida on February 19, 2014.

“…My message to you today is a tough one. I don’t expect a standing ovation when I leave. But I do want you to understand our perspective. I would be remiss if I did not share it with you … if you choose to operate in this space (mortgage servicing), the fundamental rules have changed forever. It’s not just about collecting payments. It’s about recognizing that you must treat Americans who are struggling to pay their mortgages fairly before exercising your right to foreclose. We have raised the bar in favor of American consumers and we are ready, willing and able to vigorously enforce that bar.

Ultimately, these profound changes will be good for all Americans, including industry. But please understand, business as usual has ended in mortgage servicing. Groundhog Day is over. Thank you.”

Sheriff – Update

In a June 22, 2016, Press Release, the CFPB said, in part: “In 2013, the CFPB established mortgage servicing rules designed to protect consumers against many of the practices that plagued the mortgage servicing industry during and after the housing crisis.

According to the CFPB, the rules require servicers to maintain accurate records, give troubled borrowers direct and ongoing access to servicing personnel, promptly credit payments, and correct errors on request.”

In addition to sending your RESPA letter, do not hesitate to file a complaint, with the CFPB. Click here for the particular complaint link.

The Bureau’s Enforcement Power – One Example

As an example of the Bureau’s enforcement authority, RealtySouth™, a Berkshire Hathaway Affiliate, was recently fined $500,000.00 for a RESPA violation which amounted to failure to disclose their affiliated business relationship(s) to consumers. This is a typical example of the enforcement action undertaken by the Bureau as one may readily determine with an Internet search. For those who don’t recognize the name Berkshire Hathaway, it is largely owned by one of the world’s wealthiest persons. Clearly, wealth does not buy immunity from the CFPB.

Exceptions to QWR: Those transactions excluded from the QWR are limited to “(1) subordinate lien loans or (2) open-end lines of credit subject to TILA, whether secured by a first or subordinate lien.”* Further, “(a) request does not constitute a QWR if it is delivered to a servicer more than one year after either the date of transfer of servicing or the date that the mortgage servicing loan was paid in full, as applicable.”*

NOTICE: I am not an attorney nor am I providing legal advise. This post is for educational purposes only. The images are for illustration only and not meant to imply in any way an endorsement or authorization by any government agency or authority of this blog or this post.

* Jonathan Foxx, President & Managing Director Lenders Compliance Group

Image Attribution: erickimphotography.com and CFPB

Financially Speaking™ James Spray, RMLO, CNE, FICO Pro | CO LMO 100008715 / NMLS 257365 | Rev. June 16, 2016

{kind=link}

{kind=link}