Kudos to Suzanne Woolley for authoring an article which accurately portrays how one can improve their credit.

Source: Obsessives Have Cracked the Perfect FICO Credit Score of 850 – Bloomberg

Kudos to Suzanne Woolley for authoring an article which accurately portrays how one can improve their credit.

Source: Obsessives Have Cracked the Perfect FICO Credit Score of 850 – Bloomberg

Cancelling infrequently used credit cards may seem like a good strategy, but your credit score may be adversely affected. Adam Carroll, Founder and Chief Education Officer of National Financial Educators, explains: “When you have a long-standing trade line, which is what a credit card is considered on your credit report, and you cancel that card for whatever reason, your score will actually go down as a result because one of the main impacts on your credit score is the length of credit history.” A shorter credit history translates to higher risk in the eyes of lenders.

Sean McQuay, Credit and Banking Expert at NerdWallet, agrees but includes another reason to keep older cards, noting that closing a card account results in “decreasing your overall credit line, which basically signals that a bank trusts you less.”

In addition to decreasing your overall credit line, closing an infrequently used account raises your credit utilization your total credit in use compared to your cumulative credit line. High credit utilization suggests a greater chance of falling behind on payments and/or defaulting on debts.

To avoid these pitfalls, make periodic small purchases on all your open credit cards to keep them active and pay the balances in full at the end of each billing period. By keeping credit spending low, you can still address debts while getting the full benefits of your credit account.

It’s okay to concentrate most of your credit spending in one account to maximize rewards. Just use alternate accounts often enough to keep them from being closed for lack of activity.

Source: Don’t Risk Your Credit Score In Retirement – WBRC FOX6 News – Birmingham, AL

News Release

JUNE 09, 2016

Equifax, Experian and TransUnion today launched a new website, http://NationalConsumerAssistancePlan.com, to inform and update consumers about implementation of the National Consumer Assistance Plan, an initiative launched by the three companies in March, 2015 to enhance their ability to make credit reports more accurate and make it easier for consumers to correct any errors on their credit reports.

“Providing both consumers and businesses with accurate, transparent credit reports is our first priority,” said Stuart Pratt, President and CEO of the Consumer Data Industry Association, the trade association representing the consumer data industry, including the three national credit reporting agencies. “The nationwide consumer credit reporting companies are making important changes to their procedures that will improve their ability to collect accurate information, and we want to make sure consumers know about the new options available to them.”

The National Consumer Assistance Plan is being implemented over three years, and the new website will serve as a vehicle for updating consumers about changes to their ability to interact with the nationwide consumer credit reporting companies.

Changes included in the National Consumer Assistance Plan include:

The National Consumer Assistance Plan builds on other steps the credit bureaus have made in recent years to improve consumer’s ability to resolve issues related to credit reports. In 2013, the companies launched a process under which consumers can upload documents digitally to dispute how their lenders have reported their accounts to the credit bureaus.

The plan was launched after cooperative discussions and an agreement with New York Attorney General Eric Schneiderman and a group of other State Attorneys General.

Source: News Release

Source: How FICO Scores Recover After Negative Credit Info is Purged

Mom never told you as she didn’t know either

The not so Secret Formula

Use your credit cards properly to build an awesome FICO© Score. An awesome score will give you the best advantage for the best rates on insurance, credit cards, vehicle and other installment loans and home loans. As well, having a great score will give you a distinct advantage for certain employment opportunities. Having a great score will also help you to screen potential long-term partners to determine the likelihood of a successful relationship. Let’s face it, having a great score means you keep your commitments.

By way of proper use, let’s explore what it is that is rewarded by the scoring system. Two cardinal rules are never exceed using 30% of your available credit on any card in any month. Ever. Never maximize the usage of your credit limit on any card. Ever. Better is to not exceed using 20% of your credit limit. For example, the credit limit is $1,000.00. Do not exceed $300 in use and better do not exceed $200 in use. This accounts for about a third of your total credit score.

For best results, pay off the balance monthly. In addition to never maximizing the usage of your credit limit, never exceed the limit. Ever. For your best advantage do not ever close a credit card. The aging of your credit profile is essential to having a great score. The longer you have good credit, the better for your credit history and as a result your credit score. This accounts for a little more than a third of your score. In this and the previous paragraph we have discussed that which makes up about sixty-five percent of your total credit score. Such is illustrated in the following pie chart.

At each opportunity you get, or at each opportunity you can make, increase the amount your available credit. Once your credit card issuer sees you are managing your account well, they will offer to increase your credit limits so long as you have the ability to repay. Don’t be shy, after about 6 months, contact your card issuer and ask when you may qualify for an increase.

Keep in mind that a single 30-day late payment will ding your credit score by 90-115 points. Boom! The time it takes to recover from this one 30-day late payment will take from one to three years depending on your score at the time.

If you wish to take the time, the author of this article captured the reality of building a perfect score.

With all things, including credit cards, TANSTAFFL applies. TANSTAFFL was a term coined by Robert Heinlein in his 1961 novel Stranger in a Strange Land. There Ain’t No Such Thing As A Free Lunch.

Financially Speaking™ James Spray RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365 | June 24, 2016

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.

In addition to getting the best employment and the lowest interest rate on everything financed, including credit cards, home and auto loans, the prime potential partners in the dating pool are quickly thinned of those with inferior credit.

This is clearly highlighted in a post made by the Credit Slips summary of a Washington Post article which examines the working paper recently published by the Federal Reserve titled Credit Scores and Committed Relationships.

Barron’s Market Watch recently published an article titled, Nearly 40% of Americans want to know your credit score before dating. In part, this phenomena was summarized by University of Kansas Communications Professor Jeffrey Hall who stated,

By showing an interest in these three digits, people are probably being smart rather than shallow, says Jeffrey Hall, associate professor of communications at the University of Kansas. “Finances, education, and job prospects all factor into the value of a potential mate,” he says. “Assuming that people can actually interpret a credit score meaningfully, it makes sense they would think a credit score is useful in evaluating mate value.”

“…In fact, the higher your credit score, the less likely you’ll separate from your partner — and a lower score often means you’ll be less lucky in love, researchers at the Federal Reserve Board, the Brookings Institution and UCLA recently concluded.”

Your credit score has become such a popular character-meter that there are dating services based on them. A 2015 academic study found that “quality in credit scores, measured at the time of relationship formation, are highly predictive of subsequent separations.” The research suggested “credit scores reveal an individual’s relationship skill and level of commitment.” How More Americans Are Getting a Perfect Credit Score Bloomberg Suzanne Woolley, August 14, 2017.

I think it’s safe to predict that more and more people in the dating pool will become savvy to the benefit of checking one’s credit score before entertaining the possibility of a committed relationship.

ConsumerAffairs February 9, 2020: Improving your credit score might improve your love life “…Other nuggets from the survey reveal that four out of ten people — both men and women — say irresponsible spending is a bigger turnoff than bad breath. Forty-six percent of people would break up over irresponsible spending, the second biggest reason behind cheating.”

Financially Speaking™ James Spray RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365 | Published November 13, 2015 – Updated August 16, 2017 – Updated February 9, 2020

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct for your situation. This information is not legal advice and is for guidance only. You may reproduce this information in whole and not in part, providing you give full attribution to James Spray.

Source: http://bit.ly/1GN4tyG

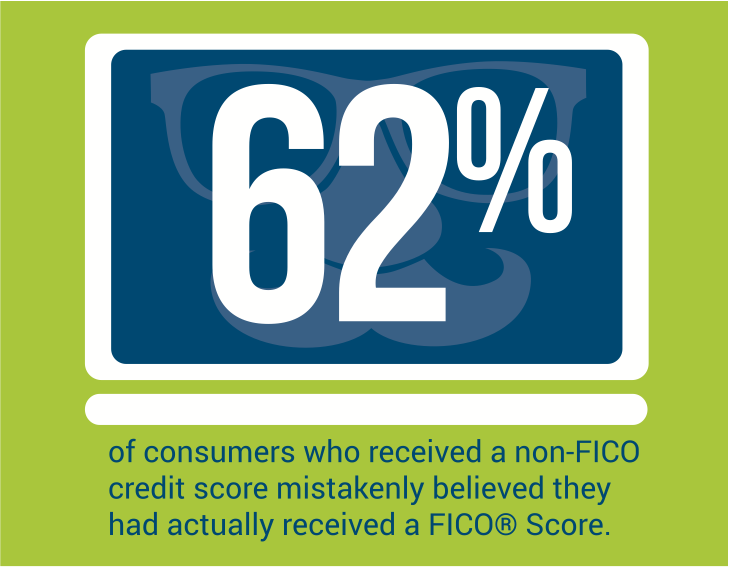

Every day consumers across America make important financial decisions, such as buying a first home. They monitor their credit score and, if necessary, take steps to improve it so that when they finally find the perfect place, they can be confident they’ll get approved for a mortgage. But often, in…

Source: When it Comes to Credit Scores, Consumers are Confused

And for additional information, Vantage Scores are no substitute for FICO Scores.

The following is written primarily for those wishing to obtain a mortgage. However the same dynamics apply to credit cards, vehicle loans, insurance, employment opportunities and even dating eligibility.

Character – Reputation is a key factor in obtaining new credit. Bankruptcy, foreclosure, late payments, settlements, collections, judgments, charge-offs and other derogatory events weigh how your credit character is measured. A short-cut for evaluating character is the credit score.

Capacity – Is the ability to repay the obligation provable with third party documentation? This is measured by the stability of the income, and how long the wage-earner or self-employed has generated that income.

Conditions – What is the purpose of the loan? If the purpose is to refinance for a rate or term improvement, a simple letter stating such suffices. If applying for a cash-out refinance, how are the proceeds to be used? Documentation is required to explain the perceived additional risk. In situations where Character is less than stellar, a cash-out refinance for the purpose, for example, reimburse a family member could jeopardize loan approval.

Collateral – How much equity is available to protect the investor? In a purchase or refinance, this is the percentage of Down Payment/Equity vs Appraised Value and the loan amount. The lower the loan amount to the equity, the stronger

For example, when the character and/or the credit are challenged a down payment/equity position of about thirty percent can mitigate two of the “C’s”. The greater the collateral/equity, a lesser weight may be given to Character, Capacity.

What is your credit score? Use this credit score simulator to find out. It’s free and it will give you a good idea of what your score range is right now.

Caution – Finally, be very wary of credit repair schemes, many are designed to part you from your hard earned money. Most of these “service providers” are scams. It’s easy to see if they are running a scam. The scammers require cash up-front; this is not legal. Pursuant to the Credit Repair Organization Act (CROA), any credit repair work must be completed before a consumer may be charged for the work. For more information, see: Credit Repair Basics.

Financially Speaking™ James Spray RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365 |October 19, 2015

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct for your situation. This information is not legal advice and is for guidance only. You may reproduce this information in whole and not in part, providing you give full attribution to James Spray.

Better job, better credit, better dating pool

We all know that a high credit score can help streamline life events like buying a house, landing a new job or a promotion or transfer and, yes, even establishing close personal relationship.

But do you know how to increase your score? Try these four moves to give your scores a boost.

Fix Credit Errors — Don’t wait for a lender to check your credit before reviewing it yourself. Request a credit report from each of the three major bureaus every year, reviewing the accuracy of your personal info, credit limits and the open or closed status of each account. Dispute any errors immediately. Understand that open/unresolved disputes will, in many cases, impede your ability to get new credit.

Ask Forgiveness — If you have blemishes on your credit, try clearing them up. Negotiate paying an old debt if the creditor will mark your account “paid as agreed.” For a late payment on a long-held account, write the creditor, acknowledge your otherwise good history and ask for a goodwill adjustment that will remove the negative item it from your credit report. Act immediately upon learning of your oversight.

Make Strategic Repayments — You may not be able to pay off your credit cards quickly, but you can strategically pay them down. Start by dividing each card balance by its limit. Demonstrate moderation to lenders by keeping your credit balance below 20 percent of your available credit limit at all times, not just once a month. If your card debts are higher, make a plan to pay the balances down to reach a more desirable ratio within a few days. This is particularly true as you prepare to apply for new or better credit.

Increase Credit Limit(s) — Another way to reduce your debt-to-income ratio is to ask for an increased limit. It’s a balancing act; keep your credit balances in check, you will earn a better credit profile resulting in a higher credit score. Your chances of getting an increase on your credit limit are vastly better while your usage of the credit limit is minimal.

What is your credit score? Use this credit score simulator to find out. It’s free and it will give you a very good idea of where your score range is right now.

Caution – Be very wary of credit repair schemes, many are designed solely to part you from your hard earned money. Further, many are just scams. You can easily tell if they are running a scam. The scammers demand cash up-front. This is not legal. Pursuant to the Credit Repair Organization Act (CROA), any credit repair work must be completed before a consumer may be charged for the work.

Financially Speaking™ James Spray RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365 | October 1, 2015 | July 8, 2018

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct for your situation. This information is not legal advice and is for guidance only. You may reproduce this information in whole and not in part, providing you give full attribution to James Spray.

Sticker shock is not uncommon for those who have not purchased or refinanced a home loan in the last 4-5 years. This post is to update the reader on the current market.

As background, the cost of an appraisal in the Denver-Metro area historically ranged from $300-$350. Typically, the appraisal was performed by a sole-practitioner, state licensed appraiser. That business model has all but disappeared for residential appraisals for lending purposes.

Given the myriad of new regulations throughout the mortgage industry, $450 $475 is now the going price for an appraisal in the Denver-Metro market.

A combination of market conditions, along with a shortage of approved appraisers, coupled with how soon one needs an appraisal, translates to a rush appraisal. A rush appraisal is defined as an appraisal report completed in less than three weeks. The cost of a rush appraisal may jump to $650.

If one lives in the mountains, let’s say Evergreen or Black Hawk, and needs a rush appraisal, expect to pay even more.

As a matter of practice, in this market, the Appraisal Management Company (AMC) gets a sizeable portion of the fee you must pay for an appraisal. In fact, the appraiser may now be paid less per appraisal than prior to the regulatory reforms. In fairness, the appraiser now gets paid for every transaction, which was not always the case prior to the enactment of Dodd-Frank and the boom of the AMCs.

The market has fewer sole-practitioner appraisers as most now work for an AMC. The AMC model has been around for decades, but due to the Dodd–Frank Wall Street Reform and Consumer Protection Act of 2010, commonly referenced as the Dodd-Frank Act, the AMC is more the norm than the exception.

There are those, whose sentiment is expressed by Sam Heskel from a recent post in the Origination News, who believe consumers would be well served by seeing a breakdown of the fees, for the appraiser and the AMC, as separate line items on the closing document.

Regarding the sticker shock, this is an entirely new mortgage lending environment. You may notice many changes, some of them very good, as you go through the process of obtaining your new mortgage.

For suggestions on what to do to prepare for an appraisal, see: Preparing for The Appraisal – Selling or Refinancing.

Financially Speaking™ James Spray RMLO, CNE, FICO Pro | CO LMO 100008715 | NMLS 257365 | September 27, 2015 | Update 8/28/16

Notice: The information on this blog is opinion and information. While I have made every effort to link accurate and complete information, I cannot guarantee it is correct. Please seek legal assistance to make certain your legal interpretation and decisions are correct. This information is not legal advice and is for guidance only. You may use this information in whole and not in part providing you give full attribution to James Spray.